Hello folks! It have been awhile since I last updated in this space, to be exact, 9 months.

Lots of things have happened to me in the last 9 months. I mean 2016 started badly for me. I was in a car accident in January and i had to pay for the damages for my family’s car repair as the quoted repair cost was lower than the excess. But as the chinese saying goes, 大难不死,必有大福 which loosely translate to ” one who survive a great disaster is destined to enjoy good fortune.”

The rest of the year indeed went on smoothly for me. I received a promotion at work and even went to U.S. for a business trip. That was actually the first time I had travel to any country out of Asia.

At the moment i am just holding on to 2 counters. STI ETF (ES3) and Frasers Centrepoint Ltd (TQ5).

| Counter | Shares | % of Portfolio | Avg. Price |

| STI ETF | 1901 | 64.37% | 2.86 |

| Frasers Centrepoint Ltd. | 2000 | 35.63% | 1.52 |

Over the course of these 9 months, I have made many buy and sell transactions.

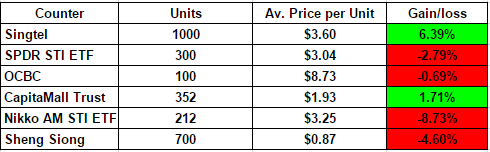

- ARA (D1R) – 7.03% Profit

- Capitamall Trust (C38U) – 9.60% Profit

- DBS (D05) – 3.39% Profit

- Singtel (Z74) – 1.10% Profit

- Sheng Siong (OV8) – 2.92% Profit

- OCBC (O39) – 1.49% Loss

- Nikko AM STI ETF – 6.63% Loss

The reason for these transaction is mainly due to SCB’s implementation of minimum commission. This forces me to offset some of my smaller holdings.

My core portfolio will mainly be index funds from now on with a mixture of individual stocks for shorter term investments.

Targets

- Accumulate STI ETF at 2.80

- Accumulate Singtel at 3.60

- Start DCA ABF Singapore Bond Index A35.